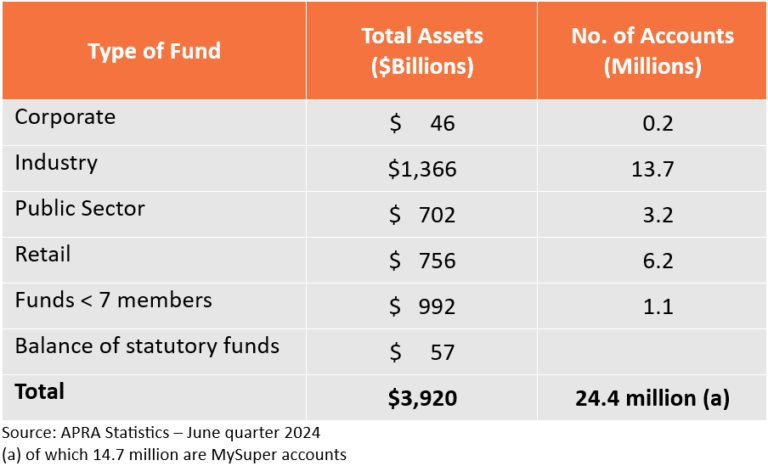

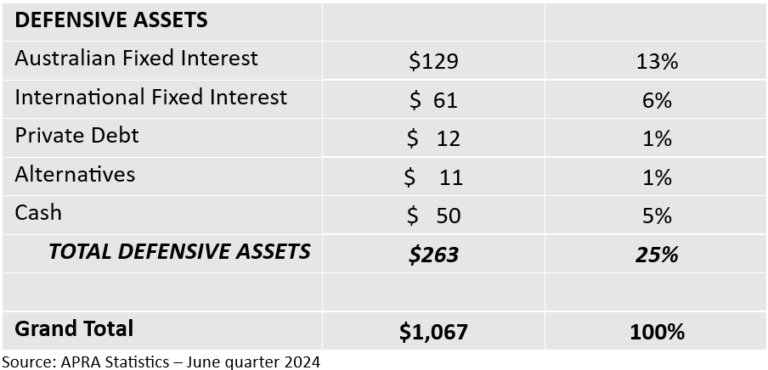

According to ASFA, Australia has approximately 24.4 million super accounts, totalling around $3.92 trillion in super assets. Of the total super accounts, 14.7 million (60%) is invested in MySuper products, accounting for around $1.07 trillion (27%) of the nation’s total pool of super assets.

These figures reflect that around 60% of workers assume that MySuper is the best investment strategy to optimise their super. Consider, however, that around 9.7 million (40%) of total super accounts equate to around $2.85 trillion (73%) of the nation’s total asset pool not invested in a MySuper product.

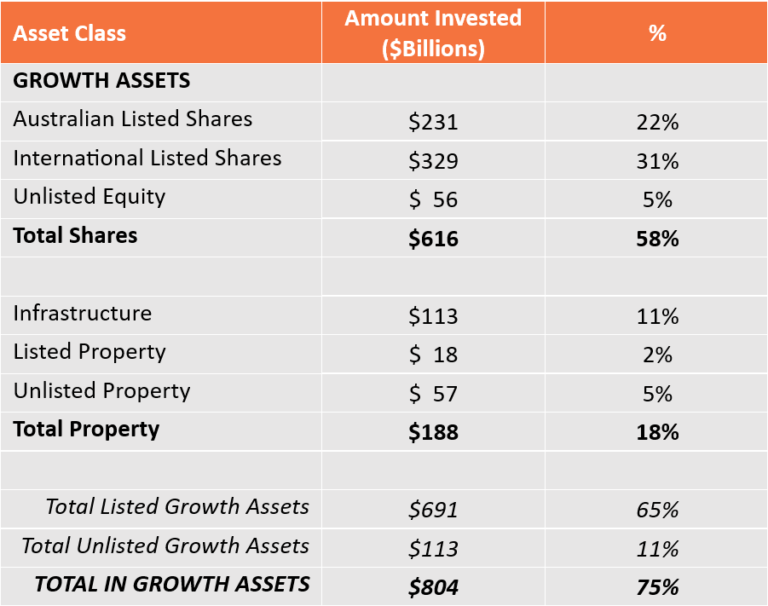

MySuper products may not be a bad option when starting in the workforce. However, they have design flaws and are possibly not ideal for those wanting to optimise super throughout their working life. The flawed design of MySuper products means younger individuals with a long investment time horizon are potentially under-exposed to growth assets, and older individuals with a shorter investment time horizon are potentially over-exposed to growth assets.

The Australian Financial Review recently reported that super fund giant AustralianSuper had to write off $1.1 billion from their private equity investments. So, understanding the exposure of MySuper products to unlisted assets and infrastructure, the level of illiquidity embedded in such investments and the level of risk is recommended.

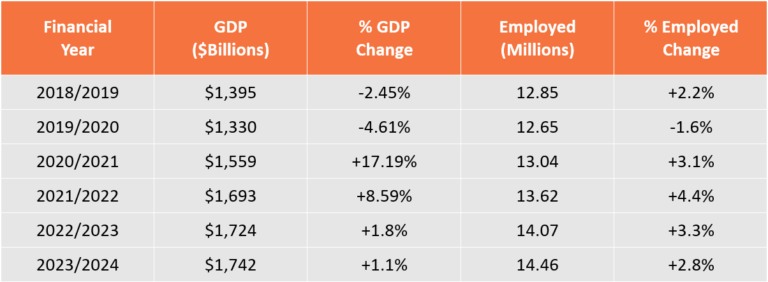

According to the Australian Bureau of Statistics, in 2020, the total number of employed people sat at 12.65 million. This number increased to 14.5 million as of February 2024 (a 14.3% increase from 2020) with a 4.2% unemployment rate. Consider the trend in employment numbers versus movements in gross domestic product (GDP) as detailed below: