PRODUCT CHOICE

Superannuation products often change in ways that you don’t hear about. A new product that enters the market or a change in existing product design can make a difference to the value of your super asset.

Determining which super product is most appropriate for you is essential, and because super is quite technical, seeking advice from a knowledgeable resource can be highly beneficial.

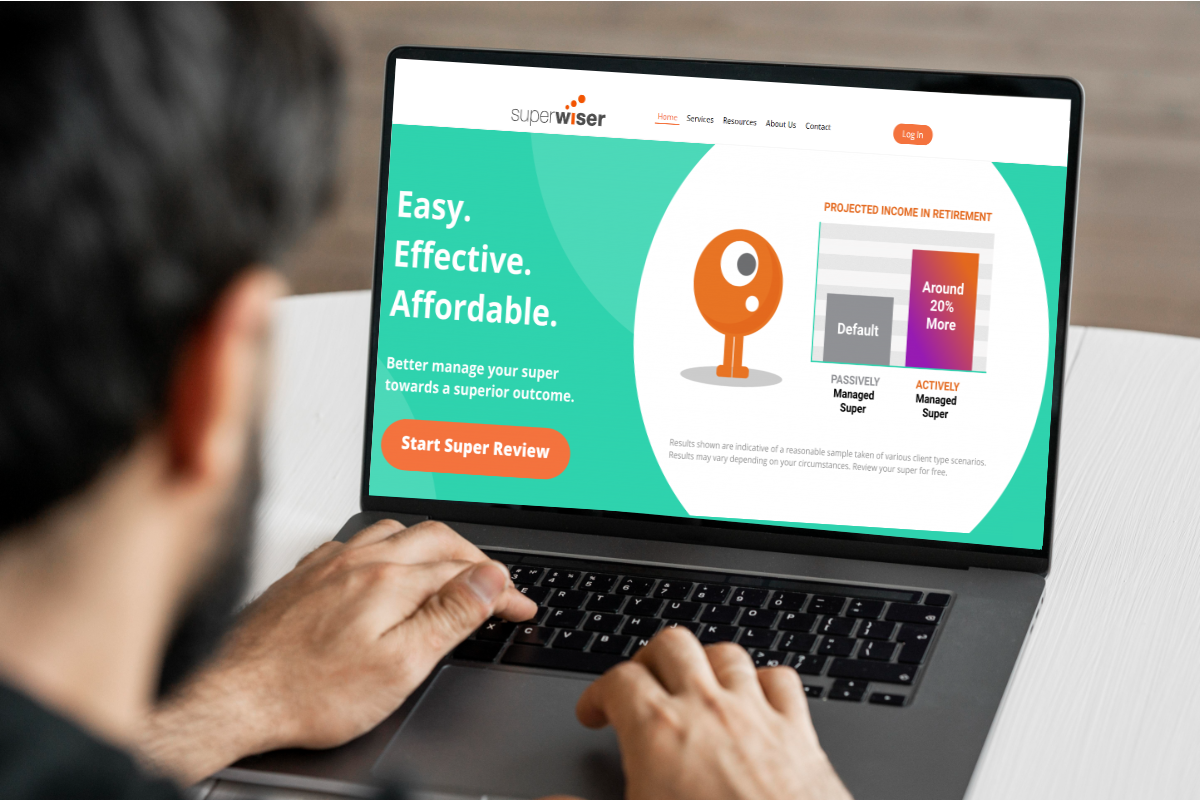

The SuperWiser client portal contains a database of over 30 well-known super products, which is constantly updated to reflect product changes, be it fees, insurance, investment choice menu or other functionality, and its purpose is to assist individuals with making informed decisions around super.

COST CONTROL

Anytime you change employer, reviewing your super fee structure is highly recommended.

Employers can often negotiate lower costs and insurance premiums for workers who join the employer super plan, so if you have not taken the time to compare your existing super product against the super plan offered by your employer, it is worth investigating.

You can complete a free super review using SuperWiser.

CONTRIBUTION STRATEGY

Every year or so, the government might change concessional and non-concessional caps, and it can be easy to miss opportunities if you are not paying attention to the impact of your contributions.

Once registered on SuperWiser, you will receive notifications of any change that might benefit your efforts to optimise your super balance.